第六章单元测试

- The excess of sales revenue over cost of goods sold is:( )。

The perpetual inventory system:( )。

- Cost of goods sold:( )。

Merchandise inventory:( )。

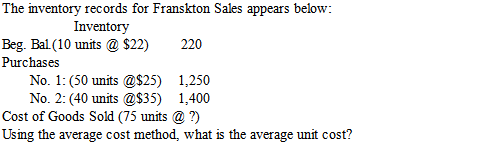

( )。

( )。- Refer to Question 5. Using the average cost method, what is the cost of goods sold?( )。

- Refer to Question 5. What value is assigned to the ending inventory, if using FIFO?( )。

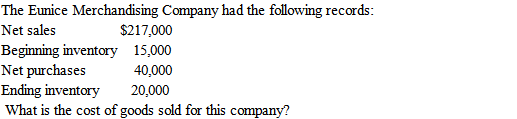

( )。

( )。- Refer to Question 8. What is the gross profit for this company?( )。

Inventory turnover:( )。

A:beginning inventory.

B:gross profit.

C:ending inventory.

D:cost of goods sold.

答案:gross profit.

A:other three choices are true. B:requires an annual count of inventory on hand.

C:is used by most businesses.

D:keeps a continuous record for each inventory item.

A:is the number of units of inventory purchased multiplied by cost per unit of inventory.

B:will be the same amount when using LIFO or FIFO, during a period of rising prices.

C:is the number of units of inventory sold multiplied by cost per unit of inventory.

D:will always be lower when using LIFO rather than FIFO, during a period of rising prices

A:is an expense on the income statement

B:both is the cost of inventory that has been sold and is an expense on the income statement C:is the cost of inventory that has been sold

D:neither is the cost of inventory that has been sold or is an expense on the income statement

A:$28.70

B:$27.33

C:$25.00

D:$22.00

A:$2,049.75

B:$2,152.50

C:$717.50

D:$1,875.00

A:$595.00

B:$625.00

C:$875.00

D:$550.00

A:$20,000

B:$35,000

C:$75,000

D:$55,000

A:$182,000

B:$35,000

C:$162,000

D:$197,000

A:other three choices are not true. B:indicates how rapidly inventory is sold.

C:is the ratio of cost of goods sold to average inventory.

D:both indicates how rapidly inventory is sold and is the ratio of cost of goods sold to average inventory

温馨提示支付 ¥3.00 元后可查看付费内容,请先翻页预览!